Healthcare’s biggest wave is just forming—diagnostics is shifting from reactive scans to continuous, AI driven prediction

- We intercept the static of survival—turning repressed murmurs into predictive medicine.

- Stop chasing symptoms. Listen to your organs before tomorrow gets louder.

Perfect Storm Market Timing

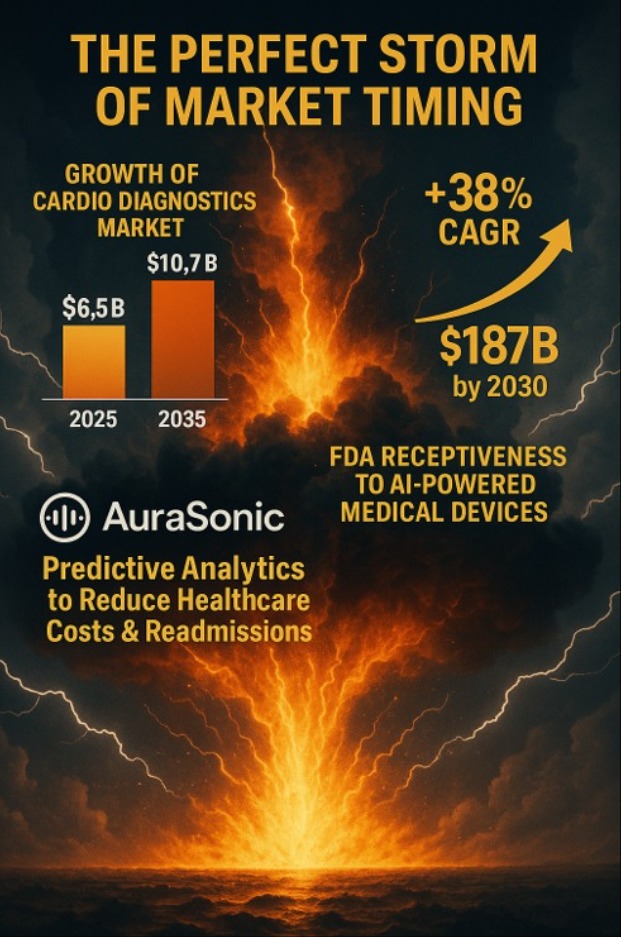

- Cardio diagnostics is expanding fast. The global cardiovascular diagnostics market is forecast to grow from $6.5B (2025) to ~$10.7B by 2035—a clear, rising beachhead for AuraSonic.

- AI-in-healthcare is exploding. Market expected to reach ~$188B by 2030 at ~37–38% CAGR, signaling massive budget reallocation toward intelligent, data-driven tools.

- Regulators are receptive—hundreds of AI devices already cleared. FDA’s maintained list shows >800 AI/ML-enabled devices authorized (882 as of Mar-2024), with ongoing updates—momentum AuraSonic can ride. ThoroughCare

- Hospitals are financially pushed to prevent readmissions. CMS’s HRRP program penalizes up to 3% of Medicare payments for excess readmissions—direct incentive for predictive monitoring that averts crises. Centers for Medicare & Medicaid Services

- Reimbursement rails already exist. RPM/RTM CPT codes (e.g., 99453, 99454, 99457; 98975–98977) enable billable remote monitoring today—accelerating adoption and shortening payback. PMCMcKinsey & Company

Unbreachable Tech & Data Moat

- Patented Smart-Skin → high-fidelity signals. Flexible inductive/capacitive/piezoresistive skins resolve micro/sub-micron motion and convert it into rich electrical data—exactly the physics our patch exploits. U.S. Food and Drug Administration

- True multimodal L-C-R sensing = unique fingerprint. Simultaneously capturing inductance, capacitance, and piezoresistance triangulates motion/pressure/strain into a data type rivals can’t reproduce without identical hardware pipelines.

- Compounding data moat. Each deployment grows a proprietary vibration corpus; in healthcare AI, model accuracy and competitive advantage scale with data volume/quality (classic data-network effects). Geisel Softwaremedcrypt.comKiteworks | Your Private Data Network

- Secure, over-the-air upgrades. Firmware/AI models update remotely—designed to satisfy FDA’s 2023 premarket cybersecurity guidance on patching & vulnerability management. U.S. Food and Drug AdministrationMedical Product Outsourcing

- HIPAA-aligned encryption by default. End-to-end AES-256 with key management aligned to NIST recommendations delivers “addressable” HIPAA Security Rule encryption and breach-safe-harbor benefits. The HIPAA JournalPMC

- Self-calibrating precision. On-device drift compensation for temperature/sweat/motion preserves hospital-grade accuracy over time—techniques proven in MEMS and acoustic sensor literature. SpringerLinkPMC

Clear Path to Revenue & Regulation

- Near-term clearance, standard path. We’re pursuing 510(k): statutory review target is 90 days, with MDUFA-V goal ~118 days total-time-to-decision—making 12–18 months from dossier lock to first revenue a realistic plan when you include pre-subs, testing, and labeling.

- Regulators are receptive to AI diagnostics. The FDA has already authorized 800+ AI/ML-enabled devices (882 as of Mar-2024), signaling strong precedent for data-driven tools like AuraSonic’s cloud analytics. world

- Software-first platform, upgradeable by design. FDA now supports Predetermined Change Control Plans (PCCP) so cleared devices can ship feature updates within a pre-agreed scope—ideal for rolling out new analytics modules to the installed base (with additional indications pursued via follow-on filings).

- Triple-stream, recurring revenue. Hardware + disposable wraps + SaaS analytics mirrors proven med-tech “razor/razorblade” economics; note how Intuitive’s instruments/accessories make up the major chunk of da Vinci revenue—recurring utilization drives durable cash flow.

- De-risked demand line-of-sight. Pilot performance plus letters of intent lock in our first clinics and expansion upsell; next-day, cloud-delivered reports fit directly into

- Exit-ready comps & multiples. Recent med-tech deals trade around ~4–6× EV/Revenue and mid-teens EV/EBITDA; sensor/analytics platforms command premiums (e.g., Boston Scientific’s ~$3.7B Axonics take-out ≈ ~10× revenue).

Diagnostic Imaging Cost Analysis

Comparative overview of common diagnostic tools, including average self-pay costs, accessibility factors, and inherent limitations

| Diagnostic Tool | Average Self-Pay Cost (US) | Complexity & Access | Limitations |

|---|---|---|---|

|

X-Ray |

$100 per scan |

Widely available, simple |

Limited to structural imaging; not predictive |

|

CT Scan |

$395 per scan |

Requires radiation, specialist |

No early signal detection; high operational cost |

|

MRI (single region) |

$400–$2,000 avg, up to $12,000 |

Slow, costly, insurance-dependent |

Expensive and reactive; not predictive |

Exit Ready Economics

1. EBITDA & Revenue Multiples

Established med‑tech and diagnostic/device firms with $3–10M EBITDA consistently achieve ~6.7–8.3× EBITDA, while revenue multiples typically sit in the ~3.5–5× range. Only companies with recurring revenue—like SaaS, consumables, or connected models—approach 8–10× revenue or 10–12× EBITDA

2. AI/ML Premium Depends on Recurring Streams

Investor premiums of +20–30% are only justified when AI/ML analytics are tightly coupled to subscription, consumables, or SaaS revenues. Stand‑alone hardware doesn’t warrant the uplift without scale or repeat use cases

3. $50M–$100M+ Rounds Indicate Strategic Signal

Raising $50M to well over $100M in biosensor or connected diagnostics startups aligns with market expectations: investors increasingly prioritize data‑rich, sticky diagnostics platforms with longitudinal analytics and workflow integration

4. Precision Diagnostics: A Soaring Market (~13% CAGR)

The global precision diagnostics market grew to $75.85B in 2023 and is projected to reach $229.3B by 2032, operating at a ~13.1% CAGR. Growth is fueled by demand in personalized medicine, oncology, and early detection platforms